Turning 65 soon? You have a lot to consider before signing up for Medicare, but there’s no reason to be intimidated. It’s true that the process isn’t as simple as just activating a simple one-size-fits-all insurance plan anymore, but it’s a process you can navigate with confidence if you take time to learn the details in advance.

For starters, Original Medicare coverage still exists, but seniors no longer have to settle for the limitations embedded in that old-school coverage. These days, Medicare supplements are a dominating force — and a valuable lifeline — in the world of senior healthcare. Supplemental insurance plans take traditional coverage to the next level by filling in the coverage gaps that once cost patients thousands of dollars a year. Here’s a look at what you need to know to choose the right Medicare supplement for your personal situation.

Medicare Supplement Basics

Also known as “Medigap,” Medicare supplement insurance plans are specifically designed to help cover some of the costs of services not covered by traditional Medicare Part A and Part B plans. Qualifying “gap” expenses include copayments, coinsurance amounts and deductibles.

Medicare supplements work in tandem with your Medicare policy. When a provider or hospital sends a bill to Medicare, the plan pays its required share of the bill first. Your Medicare supplement then pays any of the remaining charges that qualify for coverage. For this to happen, you must have Medicare Part A and Part B and pay the separate monthly premium for the supplemental policy.

Medicare Supplements vs. Medicare Advantage Plans

Both Medicare supplements and Medicare Advantage plans provide coverage to fill in the gaps left by traditional Medicare coverage, but they work a little differently. You can’t have both types of coverage, according to the official Medicare website, so it’s important to understand all the differences before choosing.

In the simplest terms, Medicare supplement plans work in conjunction with your Medicare Part A and Part B coverage, while Medicare Advantage plans work as an alternative to Original Medicare. If you enroll in Medicare Advantage, you get your coverage benefits through that private insurer’s plan instead of through the federal government’s traditional insurance program.

Medicare Advantage offers the same levels of Medicare Part A and Part B coverage, but it usually includes prescription drug coverage — known as Medicare Part D — as well. Many Medicare Advantage plans also come with extras like dental, vision and hearing coverage along with wellness benefits like nutrition counseling and gym memberships.

As the name suggests, Medicare supplemental plans simply supplement the coverages you already have. When you enroll in a Medicare supplement, you keep your Original Medicare coverage, and it will serve as the primary insurance for paying your healthcare bills, with the supplement picking up the tab for extra costs that qualify for the plan.

Characteristics of Medicare Supplements

Medicare supplements are available through any licensed insurance company that has been approved by Medicare, but the exact companies that are available to you will vary from state to state. It’s also important to note that any standard supplemental policy comes with a guarantee for renewal, even if you already have or later develop potentially costly health conditions. As long as you pay your monthly premiums, you will continue to have your supplemental coverage.

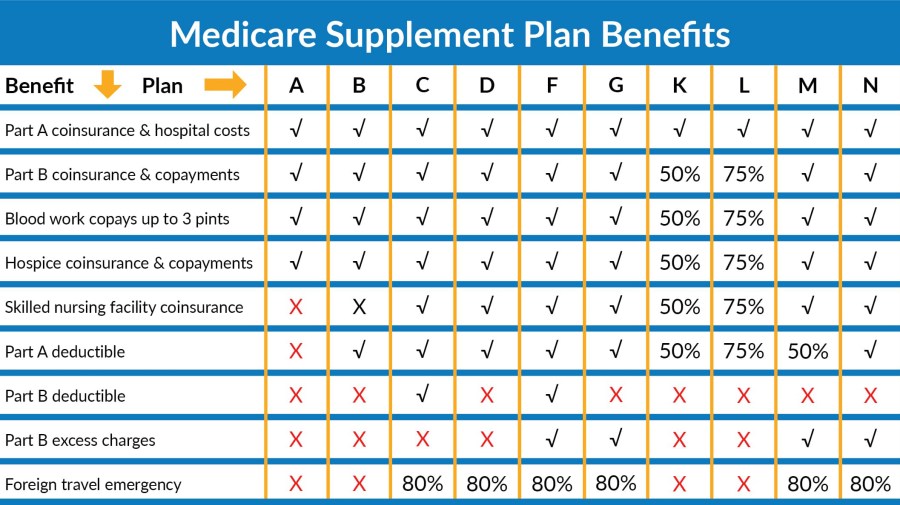

You will have numerous plan options to choose from, no matter which state you live in, and different plans will come with different coverage options. Before choosing a plan, you should decide which benefits are most important for your personal circumstances. For example, if you have chronic health conditions that frequently require expensive care, such as hospitalization, then finding a plan with the highest percentage of coinsurance payments for Medicare Part A and Part B may be your top priority.

If paying your monthly Medicare premiums already stretches your budget, then you may find it challenging to cover the cost of even the simplest medical expenses, such as doctors’ visits. If that’s the case, then you may want a supplement that pays the cost of charges that are used to meet your deductible — charges that you would otherwise have to pay out of pocket yourself.

In some very rare cases, Original Medicare covers emergency medical expenses incurred in a foreign country, but these costs are far more likely to be covered by a Medicare supplement. However, specific rules apply to different coverage plans. If you frequently travel outside the U.S., you might want to consider choosing a Medigap supplement that provides medical coverage for emergencies that occur during travel to foreign countries.

Do I Need a Medicare Supplement?

It’s not necessary for everyone to sign up for a Medicare supplement, but if you have reason to be concerned about the level of financial responsibility you could be left with after an illness or accident occurs while you’re on Original Medicare, you may want to seriously consider your options. These plans are specifically designed to help those who frequently use medical services save money by paying much less out of pocket.

On the other hand, if you don’t have any known health issues and you have rarely needed or used your medical benefits throughout your life, you may feel the cost of a Medicare supplement plan outweighs the benefits. The alternative option of choosing Medicare Advantage instead of the Original Medicare/Medicare Supplement combo is also appealing to many seniors.

Medicare Supplement Coverage Limitations

While Medicare supplement insurance does provide extra benefits to patients, these policies still don’t cover everything. For example, they don’t usually provide benefits for eyeglasses and vision care, hearing aids, dental care, private-duty nursing or long-term care. Medicare Part C and Part F are the only supplements that can be used to cover the Part B deductible, but new Medicare recipients who qualify after January 1, 2020, are not eligible to purchase plans that cover Part B deductibles, so those supplements will eventually phase out.

Insurance requirements and rules are always subject to change. Be sure to read all the benefits offered by each Medicare supplement to choose the one that best meets your needs.

Resource Links:

https://www.medicare.gov/supplements-other-insurance/whats-medicare-supplement-insurance-medigap

https://www.medicare.gov/supplements-other-insurance/medigap-travel

https://www.medicare.gov/supplements-other-insurance/how-to-compare-medigap-policies